For most North European buyers, the decision to purchase property on the Costa del Sol is years in the making. A holiday that turns into a habit. A lifestyle that keeps pulling you back. And eventually, the question that moves from the back of your mind to the front: what would it actually take to buy here?

This guide answers that question directly. Not with promotional language or approximate figures, but with a clear picture of how the process works in Spain, what it costs, what you need to prepare, and where the decisions that matter most tend to be made.

The Costa del Sol — and Marbella in particular — is not a complicated market to buy in if you approach it with the right preparation and the right people around you. But it is a market where the difference between a straightforward purchase and a protracted one usually comes down to understanding the process before you start.

Why North European Buyers Choose the Costa del Sol

Before the practicalities, it is worth being clear about what makes this stretch of coast — Marbella, Marbella East, Elviria, La Cala de Mijas, Estepona, Benahavís, and the areas in between — consistently attractive to international buyers from the UK, Scandinavia, the Netherlands, Germany, and Belgium.

The obvious answer is climate: over 300 days of sunshine a year, mild winters, and a pace of life that feels different from the moment you land. But buyers who go on to actually purchase are generally drawn by something more specific. International schools of high quality. Private healthcare that is both affordable and genuinely good. Road, rail, and air connections that make this feel less like a relocation and more like an extension of your existing life. And a property market that has, over the past decade, demonstrated consistent long-term value in the areas that matter.

In 2026, foreign buyers account for roughly 60% of all residential transactions in Marbella, and close to 40% in Málaga province as a whole. British, Dutch, and Scandinavian buyers lead the figures, drawn increasingly by the prospect of full relocation rather than pure holiday use — a shift that has been underway for several years and shows no sign of reversing.

Prices have grown 5–9% year-on-year in key areas across the coast, with prime Marbella now averaging around €5,500 per square metre in the resale market. Supply of quality properties remains constrained. For buyers who are seriously considering a purchase, timing continues to be a relevant conversation — not to create urgency, but because the window for a considered decision is rarely infinite.

What You Need Before You Begin

A number of practical requirements apply to any foreign buyer in Spain, and it is worth having these in place early — ideally before you begin actively viewing properties, and certainly before you are in a position to move on one.

NIE number. The Número de Identificación de Extranjero is a tax identification number required for all property transactions in Spain. Without it, you cannot sign a purchase deed. Applications can be made through a Spanish consulate in your home country, or in person at a National Police station in Spain. If you are working with a lawyer in Spain — which you should be — they can also process the NIE on your behalf via a power of attorney.

Spanish bank account. You will need a Spanish bank account to transfer funds for both the deposit and the final balance at completion. This is a straightforward process. Opening an account with one of the major Spanish banks takes a few days and requires proof of identity, proof of address, and your NIE number.

Independent legal representation. This is not optional, and it is not a cost to minimise. An independent property lawyer — one who acts for you and no one else — is the single most important professional in your team. They will carry out due diligence on the property, review contracts, check the Land Registry, verify there are no outstanding debts, liens, or planning irregularities, and manage the entire legal process through to completion. Legal fees on the Costa del Sol typically run to around 1% of the purchase price, which is money very well spent.

Budget clarity. In Spain, the purchase price is not the total cost. Depending on whether you are buying a resale property or a new build, you will need to budget an additional 10–13% on top of the agreed price to cover taxes, notary fees, registry fees, and legal costs. More on the breakdown below.

How the Purchase Process Works

The Spanish property purchase process is well-structured and, when properly managed, moves through four distinct stages. The typical timeline from agreed terms to completion is six to twelve weeks, though new builds purchased off-plan operate on a different schedule.

Stage One: Reservation Agreement

Once you have agreed a price with the seller, a reservation agreement is signed and a holding deposit — typically between €3,000 and €12,000 — is paid. This takes the property off the market and freezes the agreed purchase price while your lawyer begins due diligence. The reservation period is usually 30 days.

It is important not to sign a reservation agreement or pay any deposit before your lawyer has reviewed the property’s Nota Simple — the official Land Registry extract that shows the property’s registered ownership, boundaries, and any outstanding charges. This step should never be skipped, regardless of how straightforward the transaction appears.

Stage Two: Due Diligence

During the reservation period, your lawyer will conduct the full checks needed to confirm the property is free of legal issues. This includes verifying that the property is registered correctly, that there are no unpaid community fees or mortgage charges that would transfer to the buyer, and that all building works and extensions have the appropriate permits. On the Costa del Sol, where a proportion of older properties were extended or modified during the construction boom years, this last point can occasionally surface complications — which is exactly why you want your lawyer involved at this stage rather than at completion.

Stage Three: Private Purchase Contract (Contrato de Arras)

Once due diligence is complete and both parties are ready to proceed, the private purchase contract — known as the contrato de arras — is signed. At this stage, the buyer pays a deposit of typically 10% of the purchase price. The contract sets out the full terms of the sale: the agreed price, the payment schedule, and the agreed completion date.

The contrato de arras also provides both parties with a degree of protection. If the buyer withdraws without legal justification, the deposit is forfeited. If the seller withdraws, they are required to pay double the deposit back to the buyer. This bilateral commitment is what gives the contract its weight.

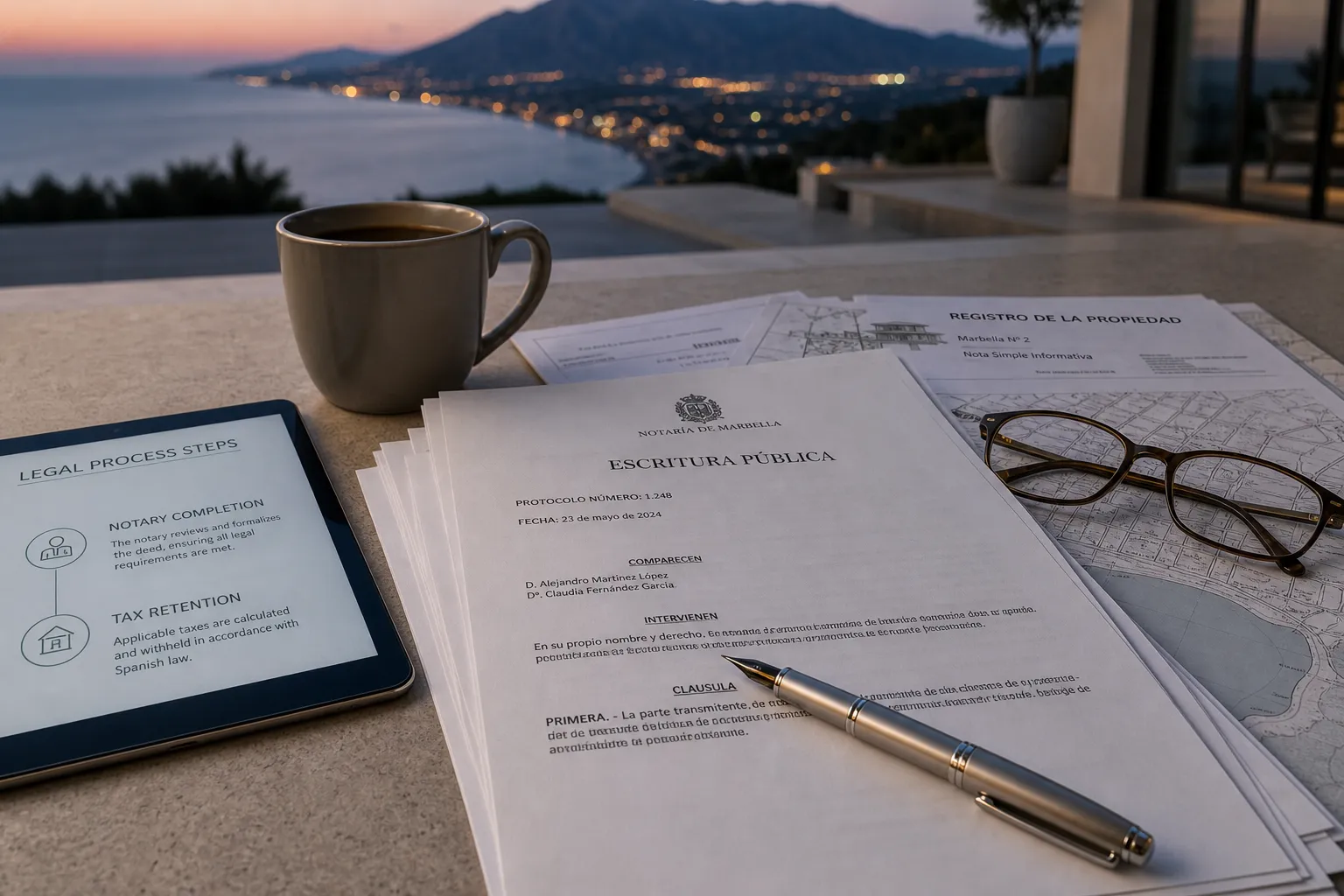

Stage Four: Completion at the Notary

Completion takes place before a notary, who is a public official responsible for verifying the transaction and formalising the transfer of ownership. Both buyer and seller (or their legal representatives, if a power of attorney has been granted) attend to sign the escritura pública — the public title deed. The remaining balance of the purchase price is paid at this stage, typically via bank draft.

If you are not able to be present in Spain at completion, your lawyer can act on your behalf under a power of attorney, which is a routine arrangement and widely used by international buyers. The process does not require your physical presence.

After signing, the notary’s office notifies the Land Registry, and the deed is registered in the buyer’s name. The buyer is also responsible for paying all applicable purchase taxes within 30 working days of completion.

Understanding the Full Costs of Buying

This is the section most buyers wish they had read before their first viewing. The purchase price is one number. The total cost of buying is a different, larger number — and it is important to understand what it comprises.

For resale properties in Andalucía:

The primary tax is the Impuesto de Transmisiones Patrimoniales (ITP), or Property Transfer Tax. In Andalucía, this is currently levied at a flat rate of 7% of the purchase price, regardless of the property’s value. This is actually one of the lower regional rates in Spain — Catalonia, for example, applies a sliding scale that can reach 11% — and Andalucía’s flat structure makes the calculation straightforward.

Reduced ITP rates exist in specific circumstances: first-time buyers under 35, buyers with recognised disabilities, and large families purchasing a primary residence may qualify for a reduced rate of 3.5%, subject to property value thresholds.

For new build properties:

New builds purchased directly from a developer are not subject to ITP. Instead, the buyer pays IVA (VAT) at 10% of the purchase price, plus AJD (Actos Jurídicos Documentados — stamp duty), which runs at 1.2% in Andalucía. The total tax burden on a new build is typically slightly higher than on a resale, but the properties are often priced accordingly.

Additional costs (both resale and new build):

- Notary fees: approximately 0.3–0.5% of the purchase price

- Land Registry fees: approximately 0.1–0.2%

- Legal fees: approximately 1%

- Mortgage arrangement costs (if applicable): varies by lender

Taken together, budget for 10–13% above the purchase price to cover all taxes and transaction costs. On a €500,000 property, that represents an additional €50,000–€65,000. On a €1.5 million property, the same logic applies. These are not figures to refine later — they should inform your initial budget from the outset.

A more detailed breakdown is available in the companion guide to property purchase costs in Marbella, which covers the numbers across different price brackets with worked examples.

Mortgages for Non-Resident Buyers

Financing a property purchase in Spain as a non-resident is entirely possible, but the terms differ from those available to Spanish tax residents. Non-resident buyers can typically access mortgage financing of up to 60–70% of the property’s assessed value (the bank’s own valuation, which may differ from the purchase price). Spanish tax residents can generally borrow up to 80%.

In practical terms, this means arriving with sufficient cash to cover the deposit, taxes, and closing costs before considering mortgage financing. As a guide: if you are purchasing a property at €600,000 with non-resident financing of 65%, you would need approximately €210,000 in cash for the deposit portion, plus €66,000–€78,000 for taxes and costs — a total of around €276,000–€288,000 in available capital before the mortgage covers the rest.

Spanish mortgage rates in 2026 remain competitive by European standards, particularly on fixed-rate products for international buyers. Your lawyer or a local mortgage broker who specialises in non-resident lending can advise on current lenders and rates. It is worth noting that Spanish banks will conduct their own property valuation as part of the mortgage process, which takes time — factoring this into your timeline from the beginning prevents delays later.

Choosing Where to Buy on the Costa del Sol

The Costa del Sol is not a single market. It is a series of micro-markets with distinct characters, price points, and buyer profiles. Where you buy matters as much as what you buy, and the right area depends on your priorities — lifestyle, schools, access, long-term value, or a combination of all four.

Marbella remains the anchor of the coast: internationally recognised, liquid, and consistent in its appeal to buyers seeking quality of life alongside asset value. The Golden Mile, Nueva Andalucía, and the area around Sierra Blanca represent the traditional luxury heartland. Marbella East — particularly Elviria — has established itself as the preferred address for international families, combining beachside living with proximity to some of the best international schools on the coast.

Further west, Estepona has transformed significantly over the past decade and now offers genuine lifestyle quality with lower entry prices. The Golden Triangle — Marbella, Benahavís, and Estepona — is a useful frame for understanding how these three municipalities complement each other from an investment and lifestyle perspective.

East along the coast, La Cala de Mijas and La Cala Golf offer a more residential, day-to-day quality of life that appeals strongly to families and buyers prioritising walkability and neighbourhood feel over resort-style amenity. Higuerón, further east near Fuengirola, represents the modern, service-led end of the market: contemporary residences with hotel-level amenity, appealing particularly to buyers who want a lock-up-and-leave property that is also genuinely liveable.

A more detailed comparison of these areas — including what they offer buyers at different price points and with different priorities — is covered in the guide to the best areas to buy property in Marbella and Marbella East.

Working With an Advisor on the Costa del Sol

There is a structural difference between searching for a property and making a considered buying decision. The Costa del Sol has no shortage of listings, portals, agencies, and individuals who will be happy to show you properties. What is harder to find is discreet, independent guidance from someone who understands the full picture: market conditions, area dynamics, off-market opportunities, realistic price expectations, and the due diligence process.

An independent buyer’s advisor does not represent the seller. They are not incentivised to move you towards any particular property or developer. Their role is to help you understand the market, define the right criteria, work through the areas that genuinely suit your situation, and structure the purchase in a way that protects your interests — from initial search through to completion and beyond.

For North European buyers who are working across time zones, managing the process at a distance, or making a decision of this scale for the first time in Spain, that kind of support is not a luxury. It is how good decisions get made.

Common Questions from North European Buyers

Do I need to be in Spain to buy? No. Your lawyer can handle the entire process under a power of attorney, and many international buyers never attend completion in person. You will, however, need to visit Spain at some point to open a bank account — or authorise your lawyer to do so on your behalf in advance.

How long does the process take? For a resale property, six to twelve weeks from reservation to completion is typical, assuming due diligence proceeds cleanly. For a new build, the timeline depends on the construction stage and the developer’s schedule.

Can I buy in Spain as a UK citizen post-Brexit? Yes. British citizens can purchase property in Spain without restriction. The practical implications of Brexit relate primarily to residency rather than ownership: if you wish to spend more than 90 days in any 180-day period in Spain, you will need to apply for a visa or residency permit rather than relying on tourist rules.

What is the Golden Visa, and is it still relevant? Spain’s Golden Visa programme — which offered residency in exchange for property investment above €500,000 — was officially closed to new applications in April 2024. It is no longer available as a residency pathway for property buyers.

Are there running costs I should factor in? Yes. Beyond the purchase, expect annual property tax (IBI), community fees if applicable, non-resident income tax if you are not a Spanish resident, and standard utility and maintenance costs. Your lawyer can model these for your specific property as part of the acquisition process.

The Next Step

Buying property on the Costa del Sol is a significant decision — financially, practically, and in terms of what it means for how you want to live. The process itself is manageable with the right guidance. The variables that matter most are usually not the paperwork, but the clarity of your criteria, the quality of your team, and the confidence that you are looking in the right places.

If you are at the stage of asking serious questions — about areas, about timing, about what a realistic budget actually gets you in today’s market — that is exactly the kind of conversation worth having before you start spending time on viewings.

Get in touch with Mikael to discuss your situation, your priorities, and where to start.

Mikael Hansen is a Costa del Sol real estate advisor working with international buyers, investors, and families relocating to Marbella and the surrounding prime areas. His work combines local market knowledge, area-specific insight, and a practical understanding of how different parts of the coast fit different lifestyles, priorities, and long-term plans.